Why Price-To-Earnings Ratios Are Less Meaningful Than In The Past And Will Be Even Less So In The Future

Introduction

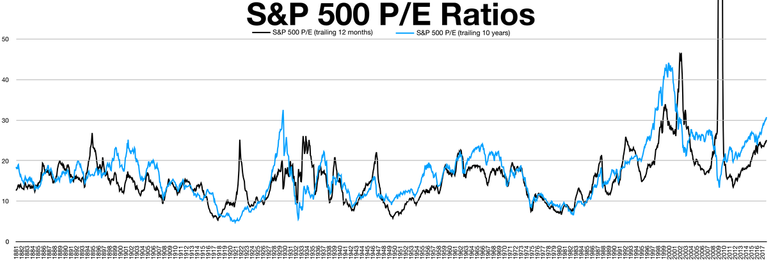

Price-to-Earnings (P/E) ratio means the ratio of the earnings per share of a company to the price of its stock. P/E ratios have traditionally been a useful measure of how over or undervalued a stock is. It still makes a lot of sense to value a company like, say, Unilever or Coca-Cola based on its current earnings. Those companies are large and established producers of every day consumer goods, food products in particular, or particularly carbonated and colored sugar water in case of Coca-Cola. There is nothing rapidly changing or high-tech in their product lines. The success of these companies is largely about logistical efficiency and marketing.

{kind=link}

There are two fundamental reasons why P/E ratios are less relevant now than they have been in the past.

Quantitative easing programs of unprecedented magnitude

The massive quantitative easing programs central banks have been forced to enact in response to lackluster growth in developed economies and in order to keep debt-ridden governments, corporations and individuals from being crushed under their debt burdens. Partially the slow growth particularly after the financial crisis of 2008 has been caused by the rapid aging of the populations in the developed world and also due to a widening gap in the skills most in demand in the economy and the existing skills of the work force. Quantitative easing programs have kept key interest rates at very low levels and also involved central banks purchasing assets such as sovereign debt, corporate bonds or even stocks from the markets thus propping up their values to a large degree. The Covid-19 pandemic and responses to it have caused economies to shrink rapidly bringing about large scale unemployment but the financial market are still close to all-time highs.

Some people say based on multi-decadal technical analysis that precious metals are well positioned to enter a bull market whereas stocks will plunge. That may necessarily not be the case despite poor P/E rations on the stock markets. Millenials who will inherit the rest of the boomer generation still with us in the next decade or so have demonstrated more interest in cryptocurrencies than precious metals as investments. Also, precious metals really do nothing but act as stores of value. The cryptocurrency space, in contrast, involves technological innovation. The one thing we can pretty much count on is the accelerated returns of technology.

The growing dominance of tech stocks

The other major factor rendering P/E rations less relevant in the future is the accelerating development of information technology. It has been based on, at the moment and in recent decades, applications of semiconductor physics. The key capabilities driving information technology: computing power, memory and bandwidth are and have been growing growing exponentially. The growing power of information technology is accelerating development in every area of basic and applied scientific research and engineering. In the recent years, big data and the innovations in software engineering making use of it, in turn driving the development of AI, have been made possible by the rapid growth in the fundamental capabilities of information technology. While individual technologies such as how many transistors it is possible to fit into a certain area of a silicon wafer are already in the decelerating part of the S-curve, cutting edge research on the next potential paradigms have already been underway for some time. The big picture of information technology is still on an exponential development track.

As I mentioned, this will accelerate every field of technology and science. Increasingly, tech companies will disrupt traditional industries not yet touched by the dominance of tech and accelerating returns. It is for this reason that past returns will be increasingly less relevant when evaluating stocks. A much more important criterium is how well that company is positioned to develop and/or take advantage of disruptive technology in its field. It is no co-incidence that the weight of NASDAQ (technology stocks) has grown on the US stock market. The proper valuation of tech stocks has relatively little to do with past earnings. Evaluating stocks is increasingly becoming a matter of speculation rather than accounting. And central banks are forced to see to it that market participants have what to speculate with.

What this means for crypto

Some people have mockingly said that blockchain is a solution looking for a problem. This kind of talk sounds eerily familiar to what I used to hear in the early 1990's when I was first introduced to the Internet. Based on what people were used to it was very hard to imagine all the disruptive use cases of the Internet that had only begun to expand into the wider world from the domains of the military and academia.

What blockchain does is automated having multiple witnesses or validators to transactions or events. It's such fundamental technology that it is natural that it is hard to imagine all of its practical applications in their fully fleshed out forms, the usefulness of which the average person can easily identify. Apart from cryptocurrency, nobody knows exactly which uses will go mainstream first and in what kind of forms.

Posted Using LeoFinance Beta

I believe that when people realize even the companies with good P/E ratios were all from buybacks, gold will continue to outperform and even start to look like bitcoin when this fake b.s. monetary system comes to an end like they always do!

I like crypto and gold going forward, waiting for the reset.

Posted Using LeoFinance Beta

Yeah, buybacks have been a common feature of the market in recent times. Some companies have are bursting with cash and don't know what else to do with it and the use it to improve their ratios. It's never a sign of a healthy market if too many do too much of that.

Posted Using LeoFinance Beta

Nothing like using 80 year old metrics to analyze things in a completely different world. Few seem to realize that we are no longer in the plant, raw materials, labor world. Thus, when sizing up capital, new metrics needs to be looked at. We are not in the same realm as before.

I am doing a series on Tesla, one that is hammered because of their absurd P/E ratio. Well, when one factors in the disruption that company is doing, it is nothing in my opinion. But few look at things that way. Only when Amazon, which had a poor P/E ratio when it was priced at $400, explodes, do people realize that there was a lot more going on than realized.

As for the future progress, I think the same curve that IT went on over the last 4 decades will be duplicated in biology. We are going to see huge strides there.

Posted Using LeoFinance Beta

When you're talking about a disruptive tech company it would make no sense not to give a lot of weight to potential future earnings. Increasingly, capitalism resembles venture capitalism because future earnings are always unknowable and a matter of speculation. This is a fairly direct consequence of the accelerating returns of investments in technology development.

Posted Using LeoFinance Beta

A lot of companies PE ratios no longer matter, they're just money laundering zombies and the ones that do pay dividends are paying you in something that is depreciating so if you adjust for all this inflation you're losing so much. It's now all about holding on to see how far it can be pumped.

The more I see all these things the more I see Bitcoin becoming the only trade that makes sense

Posted Using LeoFinance Beta

I see where you are going with this. However I think PE is still a valid metric when applied across a group of established tech companies as opposed to younger smaller tech companies.

Remember when comparing a group, even tech like Apple and Microsoft, as Buffett likes to say, price is what you pay, but value is what you get. IOW a company that earns a dollar, earns a dollar whether you pay 10 per share or 30.

That's correct. But what if that company has been aggressively buying back its own stock?

Stock buybacks are a "double edged sword" (as we say meaning can be good or bad depending) As with any use of cash you hope management is acting prudently and buying back at the right time. People often sight the airlines as an example as acting poorly by buying back stock before the pandemic. Of course a global pandemic is not easy to foresee LOL.

Sure wasn't easy to foresee. Who'd know a Chinese lab would let loose the virus right then. :)